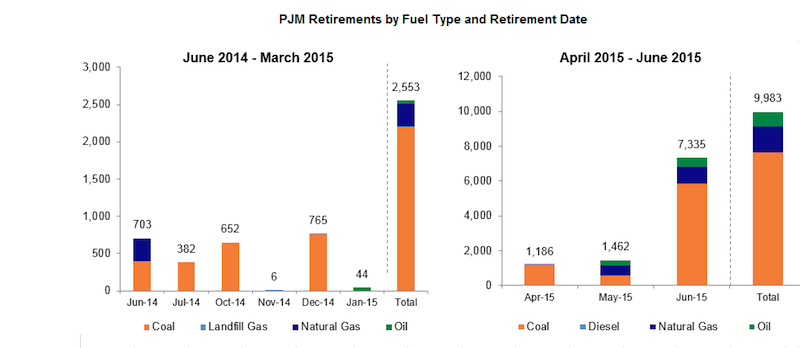

8.7 GW in upcoming PJM retirements could disrupt power markets

Over 1.4 GW of capacity is set to retire in the month of May in the Pennsylvania-New Jersey-Maryland Interconnection (PJM). These retirements are followed by another round scheduled for June 1, 2015, when over 7.3 GW of capacity is schedule to ramp offline. Should any of the units slated to retire on June 1 come offline in May, there is significant bullish risk to prices, especially during the last week of May.

Additions and Retirements

Within the last year, a number of power plant retirements and additions have changed the generation mix within the RTO. In particular, the EPA’s Mercury and Air Toxics Standards (“MATS”) and Clean Power Plan directly affect the installed capacity within the footprint. In its current form, MATS established emission standards for hazardous air pollutants from coal- and oil- fired electric utility steam generating units (“EGUs”) greater than 25 MW. The MATS rule has precipitated the retirement of a number of coal-fired plants in PJM. Since May 2014, over 2.5 GW of generation has retired within the footprint through the end of March 2015, and a number of retirements are planned for the next couple months.

The retirements that are coming in June are major baseload coal units in Western PJM, including Big Sandy (800 MW), Tanners Creek (988 MW), Muskingum River (1,400 MW), and Sporn (600 MW). Replacing some of the generation that is being retired, a few major gas-fired generators have been built since last May. These plants include Warren County (1,400 MW), West Deptford (754 MW), and Nelson Energy (628 MW). These last two units are in Eastern PJM, however the overall impact of the retirements is expected to overshadow the new builds.

Maintenance Impacts

Another critical component of the supply stack is the amount of generation that will be offline for maintenance this month. The amount of generation forecast by PJM to be on outage for maintenance in the upcoming month is comparable to what was seen last year. While projections are calling for less generation offline in Western PJM and additional outages in MidA and South, much of this change from last year is offset by new builds in the east and retirements in the west.

Gas Prices

The last crucial development since last spring has been the downward trend in gas prices. Tetco M3 is expected to average under $2 for the month similar to April, compared to an average of $3.48 in May 2015. While gas plants still often set the margin in PJM, operating costs for these plants are much lower. In some cases fuel-switching has been observed, with gas-fired generation running in place of coal units, in the off-peak in particular.

Impact on Prices

The prices represent the upper-end of expected prices for each given week in May. For example, in Week 3 prices are unlikely to average $44, however the expected supply stack and demand profile would result in at least one day where the WHUB settles at $44. In this sense the model was used to “stress test” each week’s supply stack. In general, price expectations are considerably lower than same period last year. However, Week 4 (b) in May could be considerably higher due to the potential of 7GW of generation going on retirement. Real-time and day-ahead traders in PJM should keep a close eye on the final week of May in anticipation of quite significant price swings.

Over 1.4 GW of capacity is set to retire in the month of May in PJM. These retirements are followed by another round scheduled for June 1, 2015, when over 7.3 GW of capacity is schedule to ramp offline. Should any of the units slated to retire on June 1 come offline in May, there is significant bullish risk to prices, especially during the last week of May.

Additions and Retirements

Within the last year, a number of power plant retirements and additions have changed the generation mix within the RTO. In particular, the EPA’s Mercury and Air Toxics Standards (“MATS”) and Clean Power Plan directly affect the installed capacity within the footprint. In its current form, MATS established emission standards for hazardous air pollutants from coal- and oil- fired electric utility steam generating units (“EGUs”) greater than 25 MW. The MATS rule has precipitated the retirement of a number of coal-fired plants in PJM. Since May 2014, over 2.5 GW of generation has retired within the footprint through the end of March 2015, and a number of retirements are planned for the next couple months.

The retirements that are coming in June are major baseload coal units in Western PJM, including Big Sandy (800 MW), Tanners Creek (988 MW), Muskingum River (1,400 MW), and Sporn (600 MW). Replacing some of the generation that is being retired, a few major gas-fired generators have been built since last May. These plants include Warren County (1,400 MW), West Deptford (754 MW), and Nelson Energy (628 MW). These last two units are in Eastern PJM, however the overall impact of the retirements is expected to overshadow the new builds.

Maintenance Impacts

Another critical component of the supply stack is the amount of generation that will be offline for maintenance this month. The amount of generation forecast by PJM to be on outage for maintenance in the upcoming month is comparable to what was seen last year. While projections are calling for less generation offline in Western PJM and additional outages in MidA and South, much of this change from last year is offset by new builds in the east and retirements in the west.

Gas Prices

The last crucial development since last spring has been the downward trend in gas prices. Tetco M3 is expected to average under $2 for the month similar to April, compared to an average of $3.48 in May 2015. While gas plants still often set the margin in PJM, operating costs for these plants are much lower. In some cases fuel-switching has been observed, with gas-fired generation running in place of coal units, in the off-peak in particular.

Impact on Prices

The prices in the chart below represent the upper-end of expected prices for each given week in May. For example, in Week 3 prices are unlikely to average $44, however the expected supply stack and demand profile would result in at least one day where the WHUB settles at $44. In this sense the model was used to “stress test” each week’s supply stack. In general, price expectations are considerably lower than same period last year. However, Week 4 (b) in May could be considerably higher due to the potential of 7GW of generation going on retirement. Real-time and day-ahead traders in PJM should keep a close eye on the final week of May in anticipation of quite significant price swings.

Genscape

- See more at: http://www.genscape.com/blog/87-gw-upcoming-pjm-generation-retirements-could-disrupt-power-markets#sthash.9J4Mm1sD.dpuf