Author:

Ahad Ahmed Buksh, IHS Technology

Date

07/03/2015

PDF

PDF

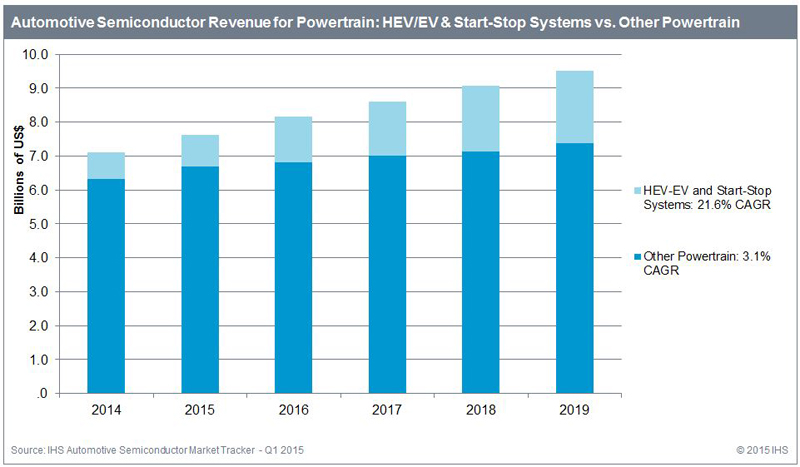

The automotive powertrain semiconductor market grew 8.3 percent in 2014, with increasing volumes of new vehicles and the need for fuel-efficient vehicle technologies the main drivers contributing to it. IHS forecasts that revenues related to powertrain semiconductors will increase with a compound annual growth rate (CAGR) of nearly six percent in the next five years from $7.2 billion in 2014 to $9.5 billion in 2019.

Advanced vehicle systems

Electrification is propelling the powertrain semiconductor market on a global scale. As an example, start-stop systems are forecast to grow at a CAGR of 21 percent, while plug-in hybrid vehicles are expected to have a strong annual growth of 37 percent for the next five years. In addition, for internal combustion engines, there is an increasing trend away from traditional incumbent multi-port fuel injection systems towards gasoline direct injection systems. Direct injection systems are more efficient and require higher semiconductor content than their multi-port counterparts. Without electrification, the powertrain semiconductor market would have only grown 3.1 percent annually for the next five years, whereas electrification is now accelerating the market at six percent growth rate annually (See Figure 1).

Click image to enlarge

Figure 1: Powertrain Semiconductor Market

Electric vehicles, hybrids leading global growth

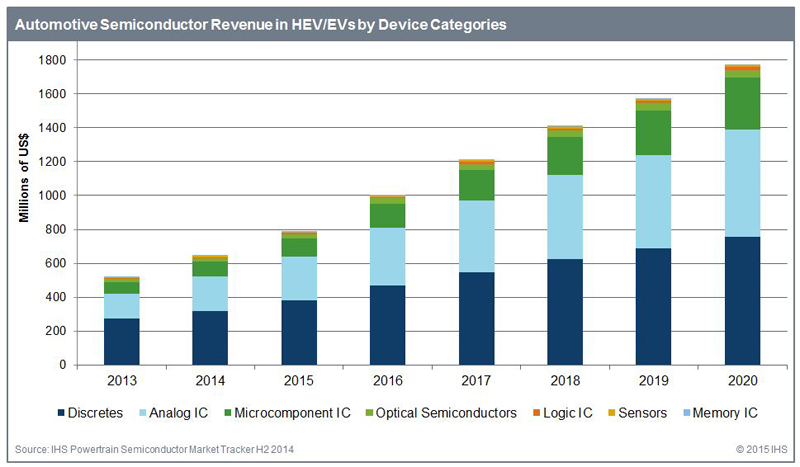

Propulsion systems for electric and hybrid vehicles demand, on average, ten times more semiconductor content than a conventional engine. Some key components include the motor inverter, DC/DC converter, battery management system and plug-in charger, all of which require power management by analog integrated circuits (ICs) and discrete components.

Growth rates are expected to be high, as the market is currently relatively small. These applications saw growth of 24 percent in 2014 and another 22 percent increase is forecast in 2015, the highest of any automotive semiconductor application. From a revenue perspective, semiconductor content in electric and hybrid vehicles are expected to generate more than $1 billion in total revenue growth from 2014 to 2019, by which time $1.6 billion will be generated in this segment (See Figure 2).

Click image to enlarge

Figure 2: HEV/EV Semiconductor Market

Powertrain systems contribute to substantial growth

Emissions legislation efforts in most regions around the world are the main drivers for semiconductor sales in powertrain applications, while current concepts in engines and exhaust after-treatment systems for ICEs, together with a requirement for on-board diagnostics, require sensors for their operation. As a result, the market for semiconductors in internal combustion engines was $5.3 billion in 2014, growing to $6.2 billion in 2019.

The engine control unit (ECU) consumes most of the semiconductor content in these applications, in addition to a growing trend toward electrification of various components – including fans, water pumps and oil pumps that will further contribute to powertrain semiconductor revenues in the future.

Leading the path for growth, however, is the start-stop system, which uses semiconductor components to sense when a vehicle is stopped, and turns off the engine, thereby saving fuel and reducing CO2 output.

Transmission management systems show slight gains

Transmissions are well-established systems for semiconductors, but with recent new concepts that include higher electronics content, such as dual-clutch transmissions (DCTs) and continuously variable transmissions (CVTs) have entered the market. As a result, this portion of the semiconductor market is expected to grow from $1.4 billion in 2014 to $1.5 billion by 2019, according to IHS. Most new growth stems from the demands on microcontrollers, particularly as a result of increased sensor content featured in new transmissions. China, Japan and eventually Europe will drive the market for DCTs, while China, South Asia and eventually North America will drive the market for CVTs.

Evolution of sensors due to stringent emission targets

Under the challenging emission circumstances, the tier 1s and OEMs have devised exhaust-cleaning strategies while maintaining car performance and improving fuel consumption. These strategies comply with on-board diagnostics and functional safety level standards like ISO 26262 where applicable. The sensors per se are also more intelligent due to an inherent ability to perform self-tests.

The evolution in legislation has lead into a significant increase in the number of inputs into the engine control unit. The other, less well developed markets such as South Asia, Russia, China, Brazil, etc. also increase their use of sensors that have been previously deployed as a result of advanced U.S., Japanese and European standards, which also drives the market for pressure, speed and position sensors, among others.

Requirements lead to advancement in microcontrollers

The evolution of the sensors for powertrain has brought a development in micro-controllers. These MCUs represent the brain of the system, and with an increase in the number of inputs, the MCU needs a higher processing power in addition to more memory and higher frequency of operation.

Apart from the impact of emission standards on MCUs, new injection systems, engine principles and increase in number of forward speeds in the transmission demand different specifications. An MCU specified for the engine control unit of a diesel engine might operate at a frequency three times higher than an equivalent MCU in the engine control unit of a gasoline engine with multi-port fuel injection system.

Powertrain MCUs are undergoing evolutionary changes. In the past, a 32-bit MCU would have sufficed for all processing, but now due to increasing DMIPS and ASIL compliancy requirements, there can be now two MCUs. One of these is a 32-bit device and the other a 16-bit MCU in the engine and transmission control units. IHS believes that this architecture will soon be replaced by one multiple-core MCUs (two or more cores) in the control unit. Multiple-core MCU solutions are already available in the market. The big MCU suppliers — Renesas, Freescale, and Infineon — launched multiple-core solutions as early as 2011.

Li-ion powering the future

Today there are mainly two types of battery technologies used in hybrid/electric vehicles: nickel metal hydride (NiMH) and lithium ion (Li-ion). These batteries made up of small cells are continuously monitored using a battery management system or BMS. The state of health (SOH), state of charge (SOC) and depth of discharge (DOD) are key parameters that need to be monitored.

These two battery types have been in fierce competition in the past, but now Li-ion batteries are winning today. OEMs such as Daimler, Nissan, Honda, BMW, Tesla, Opel, Peugeot, Ford, etc. are already using Li-ion batteries for hybrid and electric models. The Toyota Prius is the most successful hybrid model by volume and has been the main driving factor for NiMH battery development.

Today, 50% of the batteries in hybrid/electric vehicles are NiMH but this share is expected to fall drastically to 11% by the end of 2020. On the other hand, Li-ion technology—which had a 42% share of the batteries in 2014—is forecasted to increase to 82% penetration by 2020. This rapid shift will dramatically affect the semiconductor market for BMS. Li-ion batteries require more intelligent control technology as the battery has to be monitored at a cell level, as compared to modular level in NiMH.