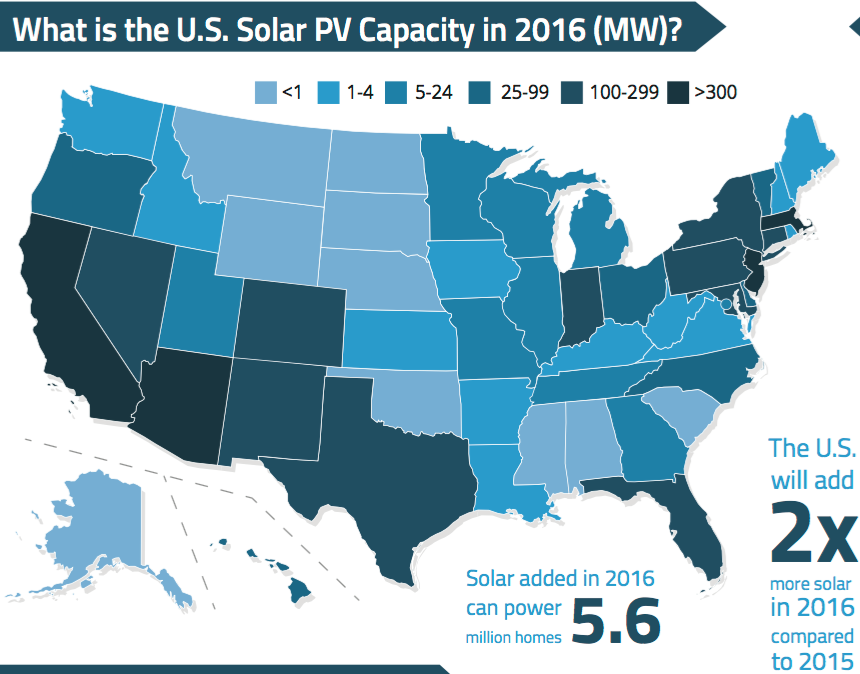

The U.S. is expected to add two times more solar in 2016 compared to 2015 thanks to declining PV technology costs, state programs, and federal incentives. Two state programs have primarily accelerated the adoption of distributed solar: renewable portfolio standards – regulatory mandate to increase renewable energy generation – and net energy metering (NEM) – billing mechanism that allows customer generators to earn credits for excess power sent to the grid.

At the federal level, multi-year extension of the investment tax credit has provided solar investors and project developers with the regulatory certainty needed to make long-term commitments and continue growth with improved access to lower cost technologies.

The growing share of customer-sited solar generation has spurred utilities to seek new methods for proper valuation of distributed generation (DG), including changes to NEM or DG tariffs to reduce utility revenue losses and share the costs with non-solar customers more fairly. Several states have initiated studies, opened dockets, or effected changes on DG valuation with regard to potential cost-shift to non-solar customers, DG aggregation, and ownership models.

Notably, Hawaii and Nevada became the first states to end retail NEM and shift to lower, wholesale-rate compensation. In contrast, California, which has the largest solar market with more than 3,000 MW on NEM tariff, has passed a successor policy which preserves the basic features of retail-rate NEM through 2019.

EnerKnol’s Primer on State of Solar: 2016 highlights major state policy actions on NEM, and more.