Legislation expanding Master Limited Partnerships (MLPS) for renewable energy categories is projected to find a path through partisan gridlock this fall. While the effect that this change in the tax code will have on renewable energies will likely be dependent on a full package of financing options to enable long-term profitability and stability, the legislation creates the possibility of at least one inroad for less expensive renewable energy financing and a step toward ultimate wind and solar grid parity.

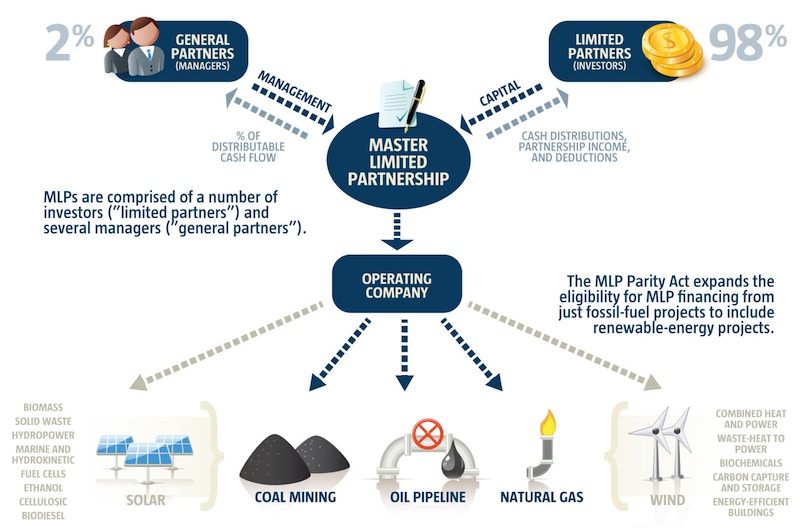

Last month, Senator Chris Coons (D-DE) testified before the U.S. Senate and Natural Resources Committee on the benefits of his Master Partnerships Parity Act (S. 795), which is designed to give investors in renewable energy projects access to Master Limited Partnerships. Rep. Ted Poe (R-TX) has also introduced an identical version (H.R. 1696) in the house. By definition, MLPs are able to raise money on public exchanges and not pay income tax at the corporate level, leading to lower capital costs.

The tax code currently restricts MLPs from investing in "inexhaustible" natural resources, such as wind and solar, while allowing investments in "exhaustible" resources, such as natural gas and coal. In 2008, Congress amended the tax code to enable MLPs to invest in alternative transportation fuels, such as ethanol, methanol, and biodiesel.

The proposed bills would further amend the Internal Revenue Code of 1986 to extend MLP availability to investors in additional projects, including renewable fuels and fuel infrastructure, electricity storage, carbon capture and sequestration, combined heat and power, energy efficient buildings, renewable chemicals, gasification with sequestration, and electricity storage devices in addition to the MLP benefits already in place for fossil fuels.

Previous versions of MLP parity bills eliminated benefits to fossil fuels, but the current legislation would maintain fossil fuel benefits along with the renewable expansion.

The American Wind Energy Association, Third Way, Solar Energy Industries Association, Biomass Power Association, and other biotechnology and renewable industry groups have endorsed the legislation, and alternative energy investment companies have begun a heavy lobby campaign for the tax code change.

Committee Members at last month's hearing expressed support for the bill, calling it a simple but powerful idea to find common ground and lead clean energy forward, and the bill has avoided antipathy for renewable energy subsidies by serving as a concession to preserve MLPs for conventional energy projects during the projected tax code overhaul in the coming months.

The tax provision's impact depends on complementary and consistent support for the new technologies and industries.

The extent to which MLPs could directly benefit demonstration and pre-utility level renewable energy industries such as cellulosic or algae-based fuels, closed and open loop biomass, or some wind and solar technologies remains uncertain. MLPs currently attract investment in long-term, stable ventures with a history of strong profitability. According to the National Association of Publicly Traded Partnerships, roughly 120 MLPs are currently traded on major exchanges. The majority of these MLPs are in the oil and gas midstream sector, that is, processing, refining, and transportation in pipelines, and storage in terminals. A more limited number of MLPs are in exploration and production.

Successful MLPs tend to have stable cash flow generators over time and markets with predictable growth rates. The midstream sector for fossil fuels earns stable revenue through contracts for processing and transporting that are not affected by price fluctuations and energy policies. Although electricity from renewables is projected to grow as an energy source over the next 25 years, this growth is contingent on capital deployment to that sector. Before the MLP structure can be a consistent vehicle for capital investment, it must first have a strong, stable long-term cash flow with minimal political risk. Many renewable industries are in some way still dependent on tax credits and mandates to compete with fossil fuels, adding an additional element of risk to a renewable energy MLP that would have to be addressed. As a result, MLPs are likely to help even the playing field for renewable investments, but without demonstrated long-term supply consistency, renewable MLPs might not attract the same number of more cautious investors that fossil fuel industries, such as pipeline companies, have seen.

Inconsistency issues

Policymakers have also highlighted this variable, and specifically the role that consistent and inconsistent government intervention can play in long-term stability. According to

Senate Natural Resources Committee Chair Ron Wyden (D-OR), tax reform energy policy should try to find ways for parity that specifically includes ways to narrow the gap between sources with consistent subsidies and sources that are subject to a year-to-year see saw, such as the wind industry, which was significantly impacted by the potential expiration of the wind Production Tax Credit. Other legislative and policy options include bond offerings for clean energy, and fixed energy credits as opposed to short-term extensions.

The Master Partnerships Parity Act is expected to become law in the coming months, coinciding with a season of significant overhaul to the tax code. This confluence of policies to stimulate private investment in renewable energies could present the beginning of new opportunities for clean energy investment and in significant steps toward grid parity.

Energy Solutions Forum