.jpeg)

New report breaks down market by application, voltage range, and geography

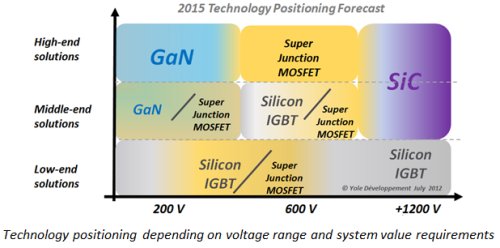

In 2012, the market for all semiconductor devices (discretes, modules, and ICs) dedicated to the power-electronics industry will reach $20 billion according to a new report, Status of the Power Electronics Industry from Yole Développement. With applications as diversified as hybrid cars, PV inverters, lighting, and energy; and voltages ranging from a few volts to a few thousands volts, power electronics is and will remain one of the most attractive branches of the semiconductor industry for the next decade. In this report, Yole provides a breakdown of market forecasts and player shares by application, voltage range, and geography for power discretes and modules, as well as wafers used for power-semiconductor device manufacturing. The power-electronics industry now deals with conversion and motion and needs lighter, smaller, cheaper, and more efficient systems. This evolution starts with improvements at the semiconductor level. Four technologies are the best candidates to handle new system requirements: Si IGBT, SJ (super junction) MOSFETs, GaN, and SiC. Already well established in the market, IGBTs account for $1.6 billion in the medium to high voltage market. Yole's report describes a trend to decrease voltage range to target consumer applications such as TVs, computer adapters, and cameras. At the same time, SJ MOSFETs in those applications present faster switching frequencies and competitive cost. Yole estimates the SJ MOSFET market will reach $567M by the end of the year. GaN and SiC also look promising to overpass silicon performance and enhance inverter capabilities. However, materials are still expensive and the technology is not ready yet. On the other hand, both of these materials can benefit from their developed status in the LED industry and Yole notes plenty of LED players paying attention to the opportunity that power electronics represent.

GaN and SiC are not mature yet for power-electronics applications: GaN requires fabrication-process enhancements, especially for epitaxy thickness. SiC is an expensive material that does yet meet the cost expectations of the consumer sector. Segmentation between technology and the power and voltage ranges will take place, driving some segments to limit their technology choices to one.

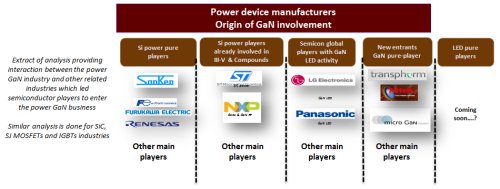

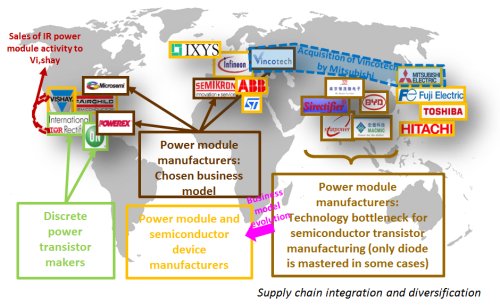

While SJ MOSFETs see new players and foundry service suppliers, the IGBT dice industry is consolidating as large players such as Infineon, Mitsubishi, and Fuji dominate some applications. However, IGBT and SJ MOSFET modules business is increasing and Yole see new players entering to supply cooling, interconnections, substrates, packaging, and gel. On the other hand, the SiC industry, which Cree has led, is now an interesting playground for new players. With access to lower cost material, the SiC industry now has the potential to ramp up. However, apart from the PFC business, technological capabilities of SiC show that it will be dedicated to high-power and high-voltage applications. Last but not least, SiC companies in China will provide competition and tougher access to local markets. At this time, the GaN industry is mostly a US business. International Rectifier, EPC, Transphorm, Microsemi, and GaN Systems now propose off-the-shelf or customized products. However, some pioneers like MicroGaN, NEC, and Powdec are showing there is a trend to globalize the GaN manufacturing industry. Meanwhile, the market is still soft and LED players are considering using their technological platform to enter this power-electronics market, which will be oriented toward low-power and low-voltage applications. The power electronics industry has great growth potential, mostly driven by energy production, distribution, and consumption, which is open and accessible, even for small players.

Because power semiconductors are just a piece of the power electronics industry, the power-semiconductor industry has to answer requirements from a bigger system: the inverter. For example, inverter manufacturers are still not implementing some expensive designs even if device and module performance are much better than those currently in production. Geographical positioning is also critical in the power-electronics area, especially with the boom in China and other emerging countries, but also because some local governments support applications such as PV, wind, and electric vehicles.