First standardization steps in the PV inverter industry

Yole Développement announces its comprehensive analysis on the first standardization steps in the PV inverter industry. Yole Développement's analysts evaluate the market forecasts and positioning of the different business players. This updated version of Yole Développement's PV inverter trends report presents a comparison between what Yole had previously anticipated and what really happened; and also the new integration that will take place in an inverter. Last year, analysts described the evolution of the 4 main parameters of an inverter; size, efficiency, cost and reliability. It can be seen in this report, that the inverter - as important as it is - is more than ever considered as the sub-system of a more important one: the PV plant. Yole Développement has also reviewed its position of some aspects, especially the micro-inverters, which the company anticipated to be more promising than what has actually appeared in 2010. PV Industry: what are the technical trends? In addition, technology development is being investigated- advanced cooling system for large size inverters, gallium nitride-based devices for conversion, laminated Busbars for conductionÖ which are all anticipated to provide promising results.

This year Yole Développement also included details on the integration of new functionalities, because it is what the company has seen all along 2010. Functionalities tend to improve the global return on investment (ROI) of the PV plant, as well as efficiency and reliability or reducing cost:

- Anti-theft

- On-site aging effect measurement

- Voltage, current, temperature monitoring

- Protection, in case of maintenance

- Communication

- Using up to 20kW inverters for installations up to 100kW

- Using large inverters for more than 100kW

- Decrease of FITs in most attractive countries (Germany, France, Italy, SpainÖ)

- Acceleration of signed contracts which has generated a shortage situation of largest PV inverter makers, like SMA, Kaco or Fronius.

- Reinforcement of US players

- Entry of other players who used to be in train or UPS business

- Arrival of Asian players, each with a competitive advantage: cost (for Chinese players), efficiency and reliability (for Japanese players).

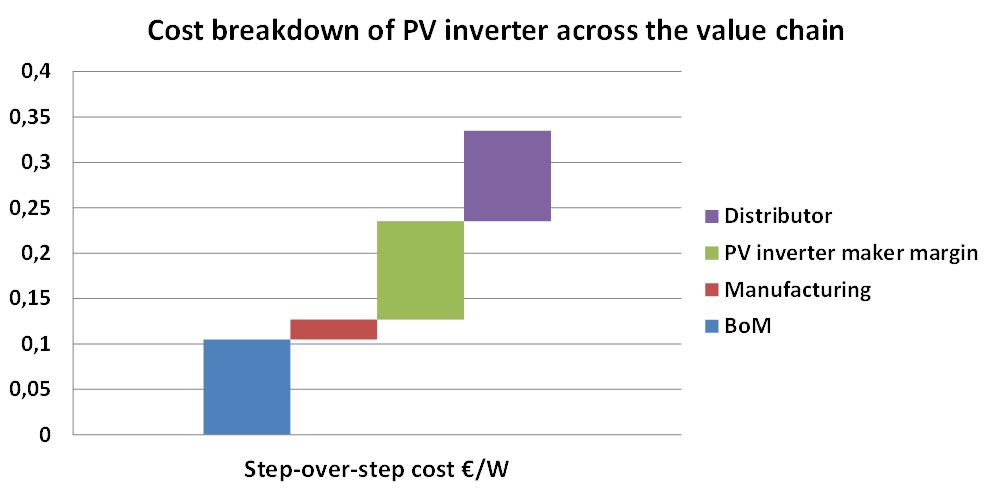

In parallel to those major events, global PV market has increased, and PV inverter market has grown as well: Yole Développement estimates it to reach €3 billion by the end of 2010, mainly driven by Europe. The USA is still growing, especially in large building installations and China has planned significant projects to fit with their expansion and to also get rid of their stock. As an opposite trend, inverter cost is decreasing considerably and today's market in Europe (from a distributor or integrator perspective) hardly accepts over 0.24€/W solutions. Chinese makers (like Sungrow) can thus easily access the market while Japanese competitors have difficulty. Another important trend that Yole Développement validated in 2010 is the newcomers' strategy to first establish in the large sized inverters and then enter the residential application: ABB, Ingeteam or Schneider are concrete examples of this. Last but not least, all the power optimization solutions are meeting issues to penetrate the market, for several reasons:

- Solutions too expensive

- Not very well defined position in the supply chain

- No clear advantages in dynamic conditions