Renewable energy prices; weather driven and volatile

Growing renewable-generation capacity reduces emissions but complicates capacity-planning and energy-pricing models

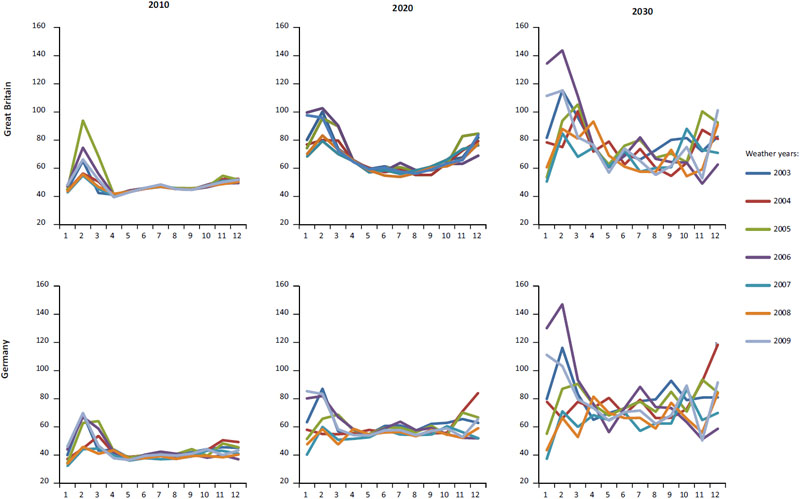

Figure 1: Wholesale energy prices will be increasingly driven by the weather.

Pöyry Management Consulting has conducted a series of studies over the last two years to investigate how European energy markets would need to evolve in the face of the radical changes expected from the introduction of renewable power sources. James Cox highlights some of the fundamental shifts expected to seen over the next 10 to 20 years if the electricity system becomes increasingly dominated by renewable and other low-carbon generation. These impacts are relevant for electricity and gas markets, given the interlinking between them. Currently the weather drives energy markets mainly as a result of temperature: Cold temperatures push up gas demand and to a lesser extent electricity demand, which in turn affects prices. Increasing amounts of wind and solar generation connected to the system will significantly increase the importance of the weather, with interactions between temperature and wind generation and between solar output and cloud cover becoming critical (figure 1). The figure highlights this increasing impact by showing monthly average electricity prices for seven different historical weather years. Each line shows the price assuming different weather patterns and plant availability, but with everything else—fuel prices, installed plant, et cetera—the same. In 2010, monthly electricity prices are only slightly affected by weather, but by 2020 and 2030, historical weather patterns lead to very different price tracks, still, cold months having much higher prices than wet, windy, warm months.

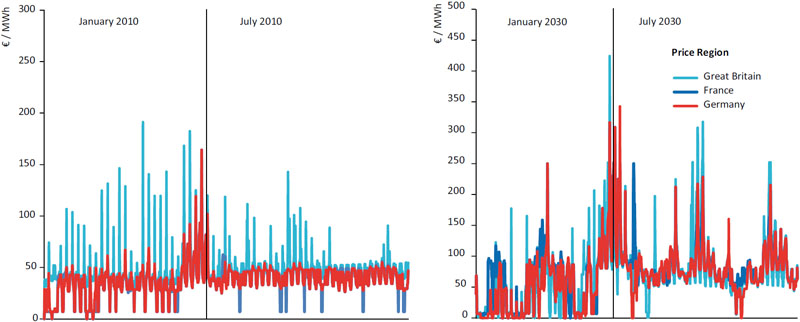

By 2030, this could mean that some customers choosing to do certain activities based on the weather. Operating washing machines and tumble dryers might become a windy weather' activity and people may defer charging electric vehicles during cold, still periods. The consequence of weather influence will be increased volatility of prices. This is driven partly by the impact of low-priced periods, when wind, solar, or nuclear sets low, potentially zero, or even negative prices. This has been seen in multiple European markets. The starkest example is Spain, where in early 2010, electricity-market prices were zero for 300 hours because of high wind and high hydro generation. Prices will also become more volatile for a second reason: fixed cost recovery. Power plants recover their annual fixed costs and their return on capital, earning profits in hours when prices are above their short-run marginal costs of generation. Increasing amounts of wind or solar generation in the system means the hours of operation of thermal plants reduce, as the plant is squeezed out of the merit order on windy or sunny days. Such plant will have to recover the same fixed costs over shorter and shorter time intervals. Prices will have to spike to high levels in these hours to remunerate the plant. Alternatively thermal plant unable to recover its fixed costs, will close down; leading to shortfalls in capacity and spiky prices, due to demand shedding. Figure 2 depicts how prices could evolve with hourly wholesale-electricity prices in three markets taken from the output of Pöyry's electricity model, Zephyr. It is clear that prices become both more volatile and riskier, with substantial periods of very low or zero prices. Intermittent thermal generation challenges investment The intermittent effect of wind and solar generation on the system is to make thermal generation intermittent in operation, with more starts and part loading, and an increasing need to operate flexibly. This is already driving changes in new plants that major turbine manufacturers are marketing, with emphasis now as much on flexibility as on efficiency—an example being the recently released FlexEfficiency50 CCGT (combined cycle gas turbine) from General Electric. More volatile prices and intermittent operation for thermal plants combine so that investing becomes much more risky, affecting the investment decision through higher hurdle-rate requirements. That could lead to capacity shortfalls, as electric-energy providers cannot economically build new generation facilities. There is serious concern in many countries that existing market designs may not be fit for purpose, witness the UK's DECC (Department of Energy and Climate Change) EMR (Electricity Market Reform), with similar ideas gaining attention right across Europe. Capacity payments (paying plant not only for energy provided, but also for its capacity) are being regularly discussed as a potential solution to ensure investment. Wholesale and retail prices likely to rise The policies embarked upon by governments will put upward pressure on the cost of electricity to consumers and taxpayers. This stems fundamentally from the cost of building renewable generation: Low-carbon generation is more expensive than conventional thermal generation. Low-carbon generation also needs support either via obligations on suppliers or subsidies in some form. One option is to levy subsidies directly on end-users, leading to wholesale prices remaining low, but end-user prices rising substantially. A second possibility is to draw subsidies directly out of general taxation, keeping both wholesale and end-user electricity prices low, at the cost of higher taxes. Another option could be the carbon price rises to act as incentive to low-carbon generation, perhaps to the extent envisaged by the UK government of £70/tonne by 2030. If there is only moderate reinforcement of interconnection, this is likely to cause both higher wholesale prices and divergence of prices between markets. This finding is in contradiction to the prevailing belief that European prices will harmonize into a single price as a result of increasing efforts to harmonize market designs. A high carbon price highlights the difference in capacity mix between countries, with countries with large amounts of thermal generation having much higher wholesale prices than those that invest heavily in renewables (though not necessarily higher end-user prices). Gas market knock-on effects On windy days, all of the Combined Cycle Gas Turbine (CCGT) power plants on the system switch off. On still days all the capacity has to switch back on again. Gas demand volatility is likely to increase, which may require additional flexibility from gas infrastructure. This could come from new fast-cycle storage facilities, or it may more transparent and liquid traded markets could release underused storage resources across Europe. The future outlined is not set in stone. A number of options could help mitigate the effects of intermittency across Europe but none of these offer a complete answer. Greater interconnection Benefits from interconnection occur by linking markets together, so the geographic area is bigger and hence the balancing of the wind is greater. The wider the geographic area, the lower is the correlation of wind. Hence the larger a market becomes, the less intermittent wind generation becomes. This is true to a point, as the output of wind farms in, say, Scotland alone is much more variable than wind farms in the whole of the UK. However, it is notable that periods of calm do extend to cover the entire North Europe region at the same time. We found wind generation across all of NW Europe together regularly drops below 5% of capacity. Interconnection allows underused flexibility in one market to be moved to where it is needed. Hydro resource—particularly in Scandinavia—is often cited as the perfect counterbalance to wind generation. The stored energy in a reservoir can be held back and released in periods when there is little wind. The balancing that hydro provides significantly reduces price volatility and unpredictability, and in the work by Pöyry, the Nordic countries always have the lowest price volatility. However, there is skepticism about Europe's ability to build interconnection between countries. It is costly, creates planning and environmental objections, and the benefits are asymmetric. Interconnecting Britain and Norway may bring cheaper electricity and flexibility, but will probably lead to higher electricity prices in Norway. Electricity storage: shaky economics The great hope for the future power system is electricity storage. The technologies on offer range through compressed-air energy storage, large-scale chemical batteries, flywheels, and supercapacitors. The value of electricity storage in a world of intermittency will rise. However, the business case for deployment of significant amounts of large-scale storage is hard to make. First, the combination of high capital costs and efficiency means that price spreads need to be significant to make a commercial return. Second, such spreads are an ephemeral, risky source of revenues, so despite potentially high revenues if market prices are volatile, the risk of low volatility is too great to allow financing of projects. Even storage built to provide ancillary services, unless there are long-term contracts in place, the commercial risk is too great. Without a radical change in cost or efficiency, financing and building large-scale energy storage is likely to remain uneconomic apart from niche applications. The exception is pumped hydro storage; in particular, where existing reservoir hydro can be re-powered, there is potential for competitive storage development. Flexible demand and smart meters: complex and uncertain The potential of the demand-side to play an active role in electricity markets has long been the hope of economists and engineers. Of the sources of flexibility available, demand-side has the greatest potential to transform, taking a potential highly intermittent, volatile, and risky world and helping to balance supply and demand and flatten prices. Despite talk of intelligent fridges and washing machines, moveable demand in most homes is very small. The two big areas for demand side are heating and electric vehicles, both of which have substantial energy requirements and a good ability to store energy. But the cost of making these transformations is significant, often only achievable in new homes due to the costs of installation. There is considerable work afoot to increase the amount of system flexibility by four other routes: interconnection, storage, demand side management, and flexible generation. But no one presents the single answer. The most likely scenario is a middle road of increased volatility, with some increase in various means of flexibility. Pöyry Management Consulting