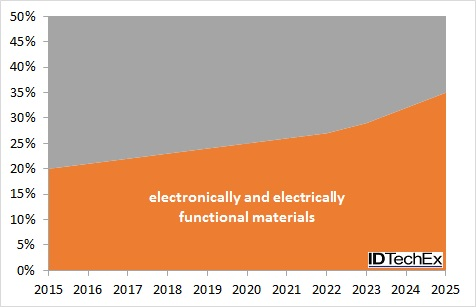

In 2025 over $25 billion will be spent on formulations and intermediate materials for wearable technology, as forecast by analysts IDTechEx in the brand new report "Wearable Technology Materials 2015-2025". Companies at this early part of the value chain will enjoy a multiplier over the coming decade. They will participate in a rapidly growing market and they will take a greater percentage of it as some other parts of the value chain are eliminated. This is not because e-fibers will be used to create e-textiles from bandages to apparel. That is a longer term prospect. Instead, it is a matter of making today's devices differently. They need to be made smaller, flexible, more comfortable, often invisibly hidden in or under clothing or transparent. Other items in the wish list will sometimes include being implantable, disposable and a frequent request is that they should never be short of electricity. Indeed, power running out after a few hours, a common inadequacy today, can be life threatening with exoskeletons and medical e-patches and dangerous with planned glucose- indicating contact lenses and wristbands for severe diabetics.

In most cases, the only way forward is to abandon the 100 year old "components in a box" approach of almost all manufacturers of wearable technology today. Instead, we shall use structural electronics where smart materials are key. This will be a cornucopia for manufacturers of electronic and electrically functional materials that can be made into structures using those increasingly crucial intermediate materials.

However, this industry needs to prioritise and de-risk its future investments and analysts IDTechEx has now provided the tools to do this. Its report, "Wearable Technology Materials 2015-2025" finds large opportunities for organics, inorganics and composites. It tackles prioritisation in different ways. First it looks at which materials are low risk because they are useful in many different ways. For example, polyvinylidene difluoride is electrically a gymnast of chemicals. It and its derivatives can be electret microphone, ferroelectric memory, piezoelectric energy harvester and much more besides.

Then IDTechEx has looked at the prevalence of different formulations that are being used in planned integrated devices for the future. For example, there is great interest in lithium, indium and titanium salts across a broad sweep of functionality. III-V compounds feature strongly in next generation products such as flexible displays and photovoltaics for low light conditions. Carbon allotropes are very broadly researched for wearables and allied markets but there is not much on C60 buckyballs. Graphene is of more interest for future batteries, supercapacitors, flexible displays and so on.

Most of the world's leading companies making primary and intermediate materials will be using IDTechEx prioritisation tools to capture a major share of this large new market. There are also many niche opportunities for smaller players such as those specialising in the chemistry of tungsten or tantalum, where many new uses are emerging. Similarly, although fluorocarbons have large potential, there are plenty of niche opportunities for other organics and some very big ones. IDTechEx counsels that many new morphologies and formats are needed from electronic printing inks to metal feedstock for the new higher speed, lower cost 3D printing. These challenges with the new formulations identified reduce competition and open up opportunities for premium pricing.