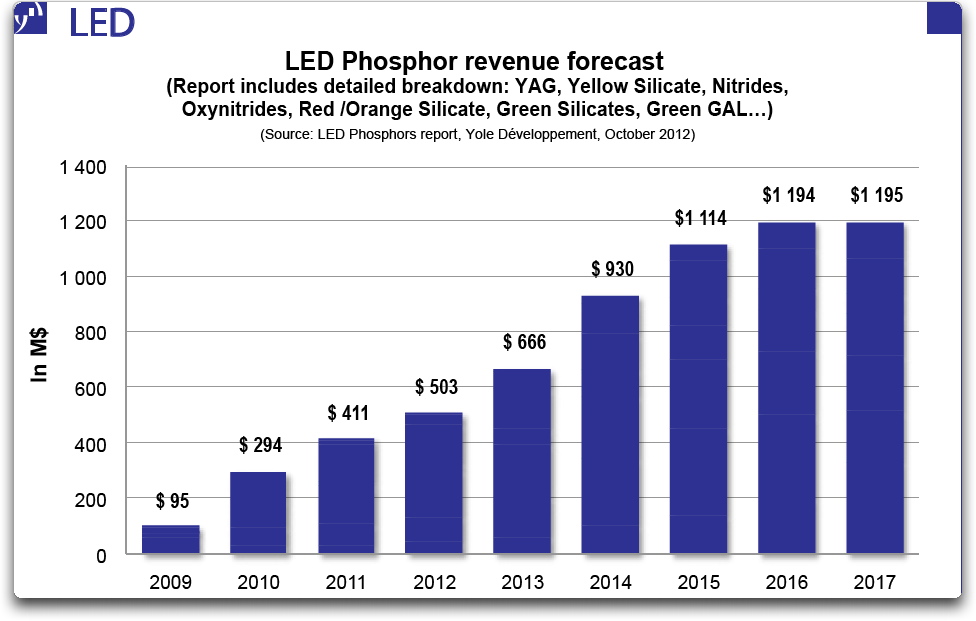

Yole Développement reports LED-phosphor market to more than double by 2017

Phosphors are a keystone of LED technologies, enabling the conversion of the monochromatic blue or near-UV light emitted by LED chips into a richer spectrum of color approaching or exceeding that of other artificial light sources. Yole Développement's new report LED phosphors provides a detailed description of the LED phosphor industry including an extensive list of manufacturers, an analysis of established and emerging composition and deposition methods, and detailed quantifications. It also provides an analysis of major technology trends like the emergence of remote phosphor, QDs (Quantum Dots), and the market dominance of IP and its limit in tenure. Due to its potential impact on the LED phosphor industry, the rare-earth supply crisis and future supply and demand trends are analyzed in detail, with an emphasis on the elements that are critical for the fluorescent and LED lighting industries. Overall, Yole Développement expects the phosphor market to grow significantly during the next five years, and potentially pass the $1 billion mark by the end of this period. However, a significant fraction of this market will remain captive, writes the report author Dr Eric Viery. The report provides ASP (average selling price) trends and detailed forecasts by phosphor type and composition.Technology is still a key opportunity for differentiation to increase performance and design in the face of a strong and limiting IP. YAG phosphor and blue LED remains the combination of choice for applications where high CRI and warm color temperature are not required, but Nichia's strong IP limits access to YAG to selected partners and major LED manufacturers that have been able to negotiate cross-license agreements thanks to their own strong IP position. While still not on an equal footing with YAG in terms of performance, silicates have improved significantly and are closing the gap. However, as Nichia's critical IP is set to expire in the next few years, an increasing number of phosphor manufacturers are offering YAG compositions as well. The next LED battle is for warm colors The next battle in the LED phosphor industry stems from the rapid growth of LED applications that require warm colors and saturated reds in display or residential and retail lighting. For these, additional red or green phosphors are added to the mix. Nitrides and Oxynitrides offer excellent performance but are both controlled by Denka and Mitsubishi Chemicals, with strong IP obtained from NIMS. Market price for these materials is 5 to 10 times higher than that of yellow phosphors. Multiple organizations are, therefore, scrambling to develop better, cheaper, and non IP-restricted compositions. Tungstates, molybdates, carbidonitrides, green Aluminates and Selenides are being investigated. In addition, QDs are finally emerging as a credible alternative to traditional phosphor in some applications. "But phosphor composition is not the only key factor. Manufacturing technology, deposition methods, and system design all have significant impact on LED and overall system cost and performance", explains Dr Eric Virey. This report provides a detailed list of established and emerging compositions and deposition technologies. Yole Développement