Yole predicts the power industry will go “inverter-centric”

Inverters will remain a key R&D focus for power electronics for the next 5 to 10 years! The power electronics industry becomes “inverter-centric” because of:

• The adoption of electrification in the transportation (from car to busses to trains and planes)

• The need for power conversion optimization for CO2 emission reduction in industrial motors for example

• And also of course the development of clean energy sources (PV, wind…) that are all big users of inverters.

These three factors are driving the inverter market to new heights, Yole Développement (Yole) expects an average CAGR for all applications to be 6% (2013 – 2020), with EV/HEV being the killer application (18.3% of CAGR). So, the overall market size of inverter applications reached about $43 billion in 2014, for 39 million units shipped for inverters. These results are part of Yole’s report, entitled: Inverter Technology Trends & Market Expectations, released in November 2014. What is also very new here, is the understanding of local market specificities, which is important to identify the most promising business opportunities.

In the past, key players were centered on their core business applications, focusing for example on photovoltaics or train. Today, there are only few examples of companies supplying the same product for several applications. But their number is increasing and this is a major strategic move of all the industry: be able to serve multiple industries, with the same knowledge. With the increase of the overall market, Yole expects a cross fertilization in-between these applications with new mergers & acquisitions or expansion strategy.

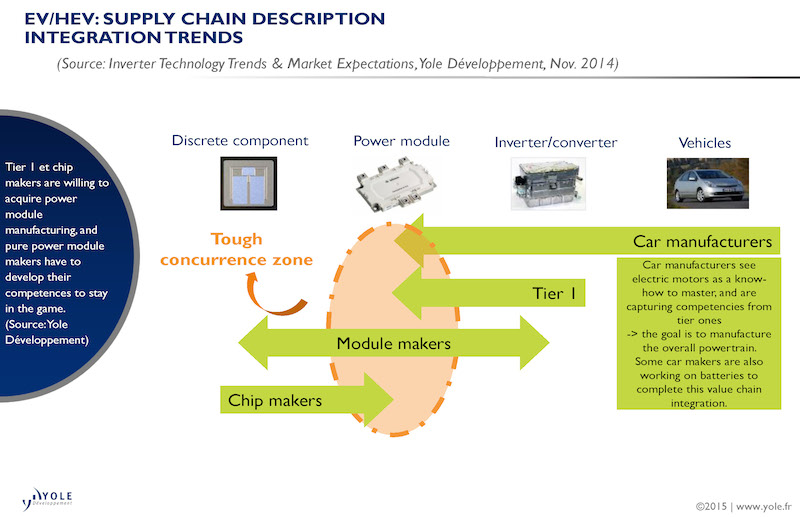

In addition to the extension of the business from one field to another (for example from train inverter to photovoltaic inverter), the supply chain is evolving in a fast move: a vertical integration and also horizontal integration are now important trends as well. Aim of this evolution is to optimize internal cost structure to better target “commodity-like” markets or offer complete solutions to customers.

Both strategies seem to be quite in opposition, but depending where you are in the supply chain, one or the other could make sense.

According to Yole’s technology & market analysis, the mega trend is really the EV/HEV penetration over the automotive industry: within the inverter market, this is definitely a huge opportunity for suppliers from neighbor applications. It will definitely impact new drivers for power electronics system integration in term of power density, weight and cost. And the new push of Toyota toward fuel cell car is just another big step toward this electrification of vehicles.

As all these changes are not done alone, several technical innovations and breakthrough are expected in inverter development to fulfil new applications needs.

At system level, power stacks will be generalized. Objective is to propose power conversion basic bricks that will be assembled together.

And of course, mechatronics is becoming key for power density, cooling optimization and system integration. That means bringing under the same roof, a lot of competencies and knowledge, from design to industrialization and manufacturing.

And major innovations are expected at power module packaging level with thermal management that will be mandatory to increase semiconductor temperature. But also low stray inductance power module for high frequency operation and passive component reduction are the key trends.

And to finish on these evolutions, even if IGBT will continue gaining shares in high voltage applications, Yole expects that Wide Band Gap devices will enable low losses converters with high power density and be a must for several of the applications. Toyota again has demonstrated on inverter using SiC devices with 80% reduction in size and weight… just incredible!

So yes, Inverters remain the key R&D focus for power electronics for the next 5 to 10 years!