Author:

Jon Cropley, Director, Automotive and Transportation Group, IMS Research

Date

08/01/2010

PDF

PDF

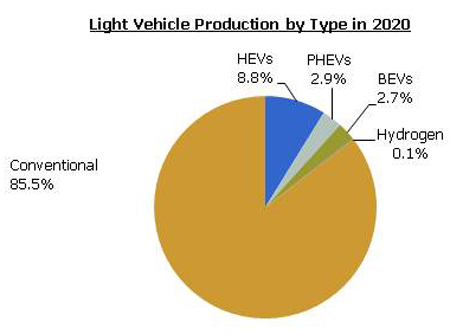

It seems like every few days a different manufacturer announces plans to introduce a new electric vehicle. While this makes it difficult for analysts like me to keep up, it's all good news for power semiconductor suppliers. The value of their products in electric vehicles is much greater than in vehicles with conventional engines. Some vehicle manufacturers already offer hybrid electric vehicles. Many others have plans to introduce them, while commercially viable plug-in hybrid and battery electric vehicles are just starting to emerge. Governments around the world are investing money to support the development efforts of the vehicle manufacturers. The Chevrolet Volt and Nissan Leaf are just two of the high profile models expected to enter volume production in the year ahead. IMS Research forecasts that demand for electric vehicles will grow steadily throughout the decade ahead from less than 600,000 in 2008 to over 12 million in 2020.

From a semiconductor supplier's point of view, growing production volumes of electric vehicles are only one side of the equation. The other side is that the value of semiconductors in an electric vehicle drivetrain is not only higher than in a conventional vehicle drivetrain: according to our research, it is over 10 times higher! Power devices account for much of this increased semiconductor content. These vehicles have significant power IC, power discrete and power module content. Much of this is for the inverter required to drive the vehicle's main motor/generators. However, many other electric vehicle drivetrain applications require semiconductors including battery monitoring and control, DC/DC converters, AC/DC chargers and air conditioning converters. Many semiconductor suppliers have so far found it difficult to enter the supply chain for electric vehicles. Japanese vehicle manufacturers have dominated production and have either used their own semiconductors or used semiconductors from suppliers they part own (Keiretsu partners). These barriers to market entry look set to disappear as vehicle manufacturers from other regions ramp up production and Japanese vehicle manufacturers look for competing semiconductor vendors. As is always the case with automotive applications, semiconductors for electric vehicles must meet demanding performance requirements and must been keenly priced. However, according to IMS Research, the market could be worth over $7 billion in 2020. As world economies struggle to recover from the recent economic downturn, this developing market could provide suppliers with a rare opportunity for substantial growth. www.imsresearch.com