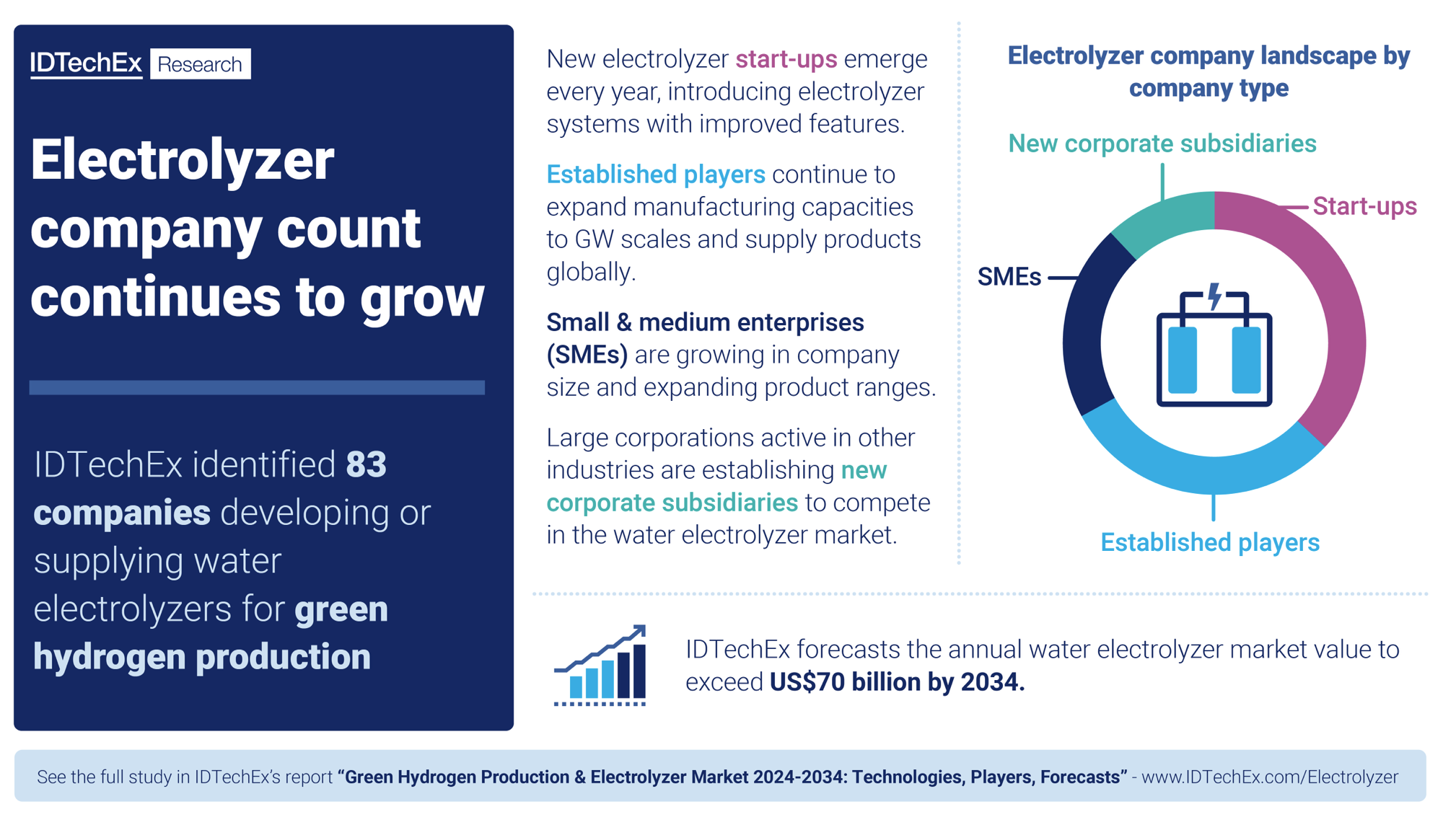

Electrolyzer Market: Consistent Uptick in Number of Green H2 Players

As green hydrogen increasingly garners recognition as a pivotal tool for decarbonizing various industries, the electrolyzer market is also observing a steady and consistent rise in the number of companies venturing into the development of electrolyzer stacks and production facilities. These companies have diverse objectives; some focus solely on supplying their core electrolyzer stack technology, while others are engaged in constructing and operating large green H2 production facilities to meet customer demands.

The overall narrative is that it is not just about the continued supply of products to the market but also the scale-up of manufacturing capabilities and improvement in electrolyzer technology on a stack and system level. A key takeaway is that as the demand for low-carbon hydrogen rises, the electrolyzer industry is set to attract more participants. This article provides a view of some overarching trends seen in the current electrolyzer market for green hydrogen production.

For context, the electrolyzer is a key unit in the green hydrogen plant, responsible for the splitting of water molecules into hydrogen and oxygen using renewable energy. There are four primary electrolyzer technologies for green hydrogen production: alkaline water (AWE or AEL), proton exchange membrane (PEMEL or PEMWE), anion exchange membrane (AEMEL or AEMWE), and solid oxide electrolyzers (SOEC or SOEL), each with distinct performance characteristics, commercial maturity, and various pros and cons.

IDTechEx's recent electrolyzer market report offers an in-depth analysis and comparison of the different electrolyzer systems available, covering mechanisms, materials, system KPIs, key industry players, commercial projects, and techno-economic considerations, along with a 10-year market forecast.

Established water electrolysis companies

Established players in the water electrolyzer market include companies that have been historically active in the industry and have developed commercial product ranges, large-scale manufacturing, and substantial commercial order pipelines.

These companies are mainly based in Europe, North America, and China and supply alkaline and PEM electrolyzer products. It is worth mentioning that alkaline and PEM electrolyzers are also the current dominating technological choices for green hydrogen plants, as the former is a mature and trusted technology while the latter is a newer technology with efficiency and dynamic capability benefits. Some examples of companies in this category include the likes of thyssenkrupp nucera (a German developer supplying alkaline electrolyzers), Plug Power (an American developer supplying PEM electrolyzers and constructing its own plants), and Peric Hydrogen Technologies (a Chinese developer supplying both alkaline and PEM systems).

Notably, Chinese companies are some of the most advanced in terms of low CapEx alkaline systems as well as gigawatt-scale electrolyzer manufacturing plants (gigafactories). European and American developers are not lagging significantly behind as demand for their products is high and some companies having established gigafactories, with many more aiming to bring those online in the next few years. IDTechEx expects the dominance of these regions in the electrolyzer market to continue due to the existing manufacturers' capabilities and relatively high interest in green hydrogen in those regions.

Corporates with new hydrogen-focused subsidiaries

Many large corporations are becoming more interested in hydrogen technologies and are either investing in the space or developing products themselves. These companies include established industrial equipment suppliers, engineering services companies, renewable energy developers, and automotive OEMs, to name a few. A notable recent example is Toyota, who have developed a PEM electrolyzer product based on their PEM fuel cell technology from the Mirai fuel cell electric vehicle (FCEV). Another example is LONGi Hydrogen from China, a division of LONGi formally established in 2021 to commercialize their pressurized AWE technology.

Such companies are based in developed economies, including Europe, China, and Japan. For many of them, hydrogen has become one of the key focus areas for future business and product development strategies. Many of these players are trying to quickly commercialize their products and establish gigafactories to gain significant market shares and compete with the already established players.

Small & medium enterprises (SMEs) and start-ups

SMEs active in the electrolyzer market are companies that have been active in the market for many years but have not scaled up to the same levels as established players. For these companies, electrolyzers may not be a main priority as they are just some of the products on offer, which is like the new corporate subsidiaries mentioned previously. For others in this space, sustainable and consistent growth with proven products is more important than the rapid growth typical of start-up companies. Some examples of SMEs active in the electrolyzer market are ErreDue and Next Hydrogen. The future may see many of these SMEs grow to become established players with large manufacturing capacities and product ranges.

The number of start-ups in the electrolyzer market indicates the high interest to develop new or improved electrolyzer technologies. Start-up players typically focus on solving problems that are seen in existing electrolyzer technologies. For instance, Hysata is an Australian company developing a new alkaline electrolyzer based on a capillary-fed cell design, which promises significant efficiency improvements by minimizing the formation of product gas bubbles that obstruct active electrode sites. Other start-ups focus on commercializing other variants of water electrolysis, namely AEM and solid oxide electrolyzer technologies. These include the likes of Versogen (US-based AEM developer) and Genvia (French SOEC developer).

Notably, many start-ups are still at technological readiness levels (TRL) of 6 to 7, as they have working pilot and industrial-scale prototypes being tested in operational environments. This is a stage where many companies fail due to a lack of commercial interest and funding as well as over-inflated ambitions, coupled with intense competition in the growing hydrogen market. Although many will fail, many will also succeed and develop into more established players.

Further insights

IDTechEx forecasts the annual water electrolyzer market value to exceed US$70 billion by 2034, representing a CAGR of 40.7% over 2024-2034. This substantial growth will be driven by an array of factors, ranging from overarching market drivers, such as national low-carbon hydrogen targets, to technological developments and electrolyzer manufacturing capacities.

IDTechEx's new "Green Hydrogen Production & Electrolyzer Market 2024-2034: Technologies, Players, Forecasts" report forecasts significant growth in the green hydrogen market, both in terms of project installations and electrolyzer manufacturing capacity, offering 10-year market forecasts in gigawatts (GW) of electrolyzer capacity and US$ billions (US$B) for the key electrolyzer technologies: AWE, PEMEL, AEMEL and SOEC. The report also includes discussion of novel electrolysis technologies (e.g. seawater & CO2 electrolysis), comprehensive analysis of electrolyzer manufacturers by state of development and commercial system specifications, analysis of manufacturing capacities technology and region, green hydrogen project case studies as well as outlooks on future electrolyzer technology adoption.