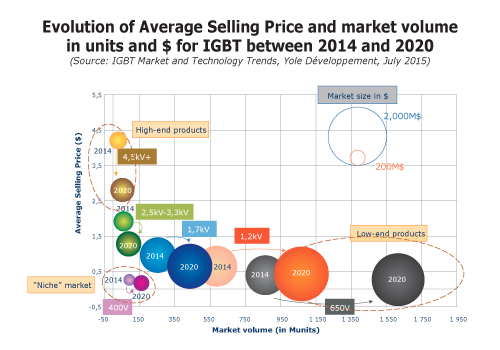

Vehicle electrification is heavily impacting the IGBT market, with huge volumes and significant added value because of the power modules used. Vehicle volume will be critical by 2018, and the IGBT market for electrified vehicles will more than triple over the next six years. By 2020, we expect electrified vehicles to represent almost 50% of the IGBT market. The first IGBT devices commercialized 30 years ago had a voltage breakdown around 1,100V. Since then, power range has broadened to 400V - 6,500V, allowing IGBT to enter all power electronics applications.

Stimulated by the electric vehicles market and its own maturity, IGBT devices is a dynamic market, with a 10% CAGR expected from 2014 - 2020. While IGBTs for the consumer and white goods markets are expected to lose market share over time, other markets, i.e. grid, photovoltaics, and UPS (driven by data center growth), are very dynamic. In terms of voltage evolution, high and very high voltage IGBTs will gain market share in the coming years.

Yole Développement has released a report that presents updated IGBT market forecasts, with a split by voltage and application. Sub-segments are also analyzed for each of the six main power electronics applications, and a comparison with our 2013 report’s market forecasts is provided.

A mature industry

Most IGBT manufacturers have been involved in the field for decades. Relationships are well-established between tiers and users, and business models are already drawn. However, evolutions are occurring: with the electrified vehicle market’s growth, the power module is becoming a key piece of the value chain and an important step to master.

More and more companies are choosing to enter the power module market in order to capture this added value. However, many challenges must be faced at the packaging level, such as yield increase, failure issue reduction, manufacturing ease, and cost competitiveness. To achieve these targets, new designs and new materials can be used, either to eliminate connection levels or improve interfaces. New solutions inspired by big-volume markets like smartphones are being adapted to higher power needs: for example, modules integrating embedded dies are beginning to enter the market via areas like photovoltaics and automotive. Big players are also pursuing M&As in order to quickly acquire know-how.

This report provides an overview of updated market share, with a split between power module makers and discrete component makers. A description of the supply chain and the companies involved is also provided for each key power electronics application.

China entering the market

In 2014, as in 2013, China represented around 1/3 of the IGBT market. Many Chinese companies are involved in module manufacturing and buy the dies from foreign companies for integration. However, we see an increasing number of Chinese companies trying to enter the die manufacturing market. Some are developing their own technology, while others are choosing to acquire die manufacturers. Regardless of their preferred tactic, every company understands that developing a reputation for good quality is key in order to first enter their local market, and then compete with established IGBT manufacturers. In this report, you will find a presentation of Chinese players split between power module makers and IGBT die makers, along with an associated power range.

In terms of market share, Japanese companies still lead, even in light of the recent merger between International Rectifier and Infineon. To answer Chinese competition, Japanese and European players rely not only on their experience and product quality, but also on a strong in-house market. With an overall market fueled by electrified vehicles, these established players can benefit from a strong local supply chain in automotive, and look forward to attractive future growth.

- small.jpg)