The term "smart grid" is widely used throughout the electronics industry. Over the last couple of years, its frequency of usage appears to have ramped up, even to the extent whereby commercials are touting grid evolution as the next big thing. In reality, these two words somehow seem inadequate in communicating the shear scale and complexity of the issue. At IMS Research we are concerning ourselves with how the smart grid trend will create additional revenue opportunities beyond what conventional grid investment provides companies involved in this infrastructure, from utilities all the way to IT consultants. Without having a broad view of the entire landscape of products and services affecting the smart grid, it's hard to measure the rate of its evolution. One method that provides a decent proxy for measuring this evolution is to look at the smart meter market, which is a key technology in the overall implementation.

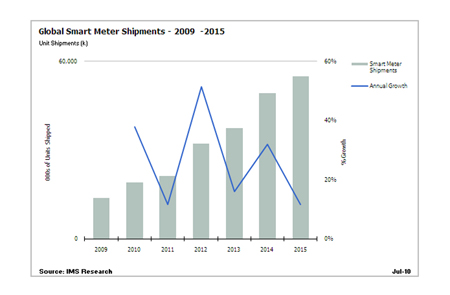

Halfway through 2010 the smart meter market is experiencing record growth globally, with IMS Research predicting some 20 million unit shipments in 2010. With over 50 million more smart meters under contract in North America, and mandates in Europe for complete nationwide rollouts, it is apparent that utilities see value in updating their respective electricity grid infrastructure with modern communications electronics and IT investment. IMS Research uses a very strict set of guidelines when reviewing the entire spectrum of advanced electricity metering, limiting our definition to any meter with the ability to remotely communicate. The booming sector of smart meters is defined as any advanced electricity meter that is installed in an infrastructure network (AMI), has two-way communication capability, and has embedded firmware in the meter itself to facilitate smart grid functions at the home, or building on which it is installed. An example of smart grid applications would be "time of use" (TOU) pricing, in which the pricing model for electricity is communicated to the customer in real-time and is altered dependent on overall electricity consumption in the neighborhood, or at the municipal level. North America and Europe are the regions where smart meter installations are currently happening, and projected to dramatically grow over the next five years; thus it makes sense that we should expect to see the largest smart grid investments here. IMS Research has also identified pilot programs in Latin America, the Middle East and Asia; however, it is currently unclear whether smart grid functionality beyond automated meter reading will be implemented in these regions. This begs the question of how else will smart grid investment take place. Home area networks (HAN) are being discussed in North America and Europe, but are these an important driver for installing smart meters worldwide? Will developing regions, with much more operational side savings to be realized, install basic two-way AMI meters only without any consideration for HAN adoption? IMS Research is working to outline a clear understanding of how the smart grid evolution is altering the electronics market and new studies, such as exploring the market for distribution (substation) automation, will be the next step to answering some of these questions. www.imsresearch.com